Roth ira vs traditional ira: which one is better in 2025?

Roth IRA vs. Traditional IRA: Choosing the Best Option in 2025

Roth IRA vs. Traditional IRA: Choosing the Best Option in 2025

Retirement planning necessitates careful consideration of various investment vehicles. Among the most popular are Roth and Traditional Individual Retirement Accounts (IRAs). Both offer tax advantages, but these advantages differ significantly, impacting long-term investment growth and tax liability. Understanding these differences is crucial for making an informed decision that aligns with individual financial goals and circumstances. The optimal choice depends on factors like projected income throughout retirement, anticipated tax brackets, and risk tolerance.

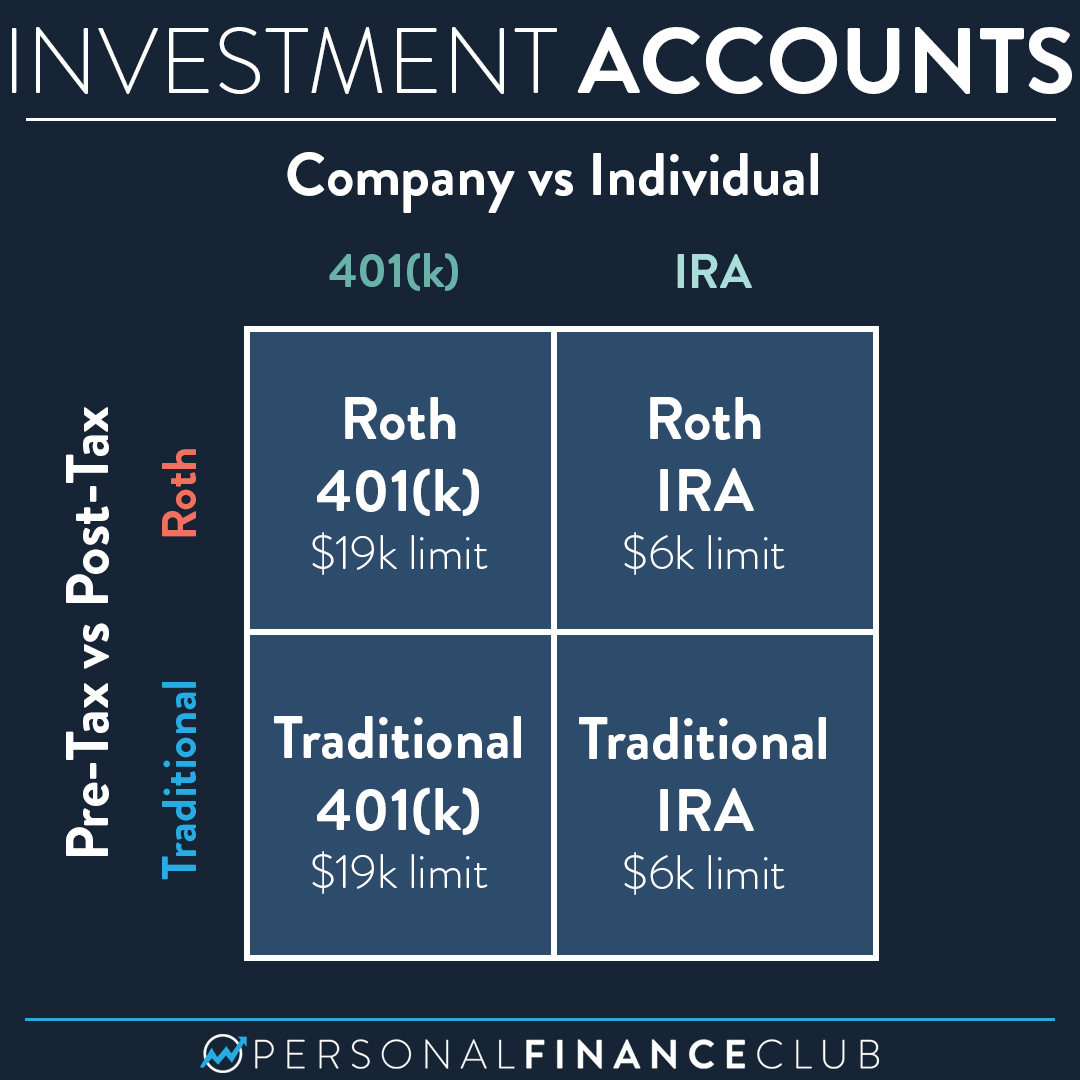

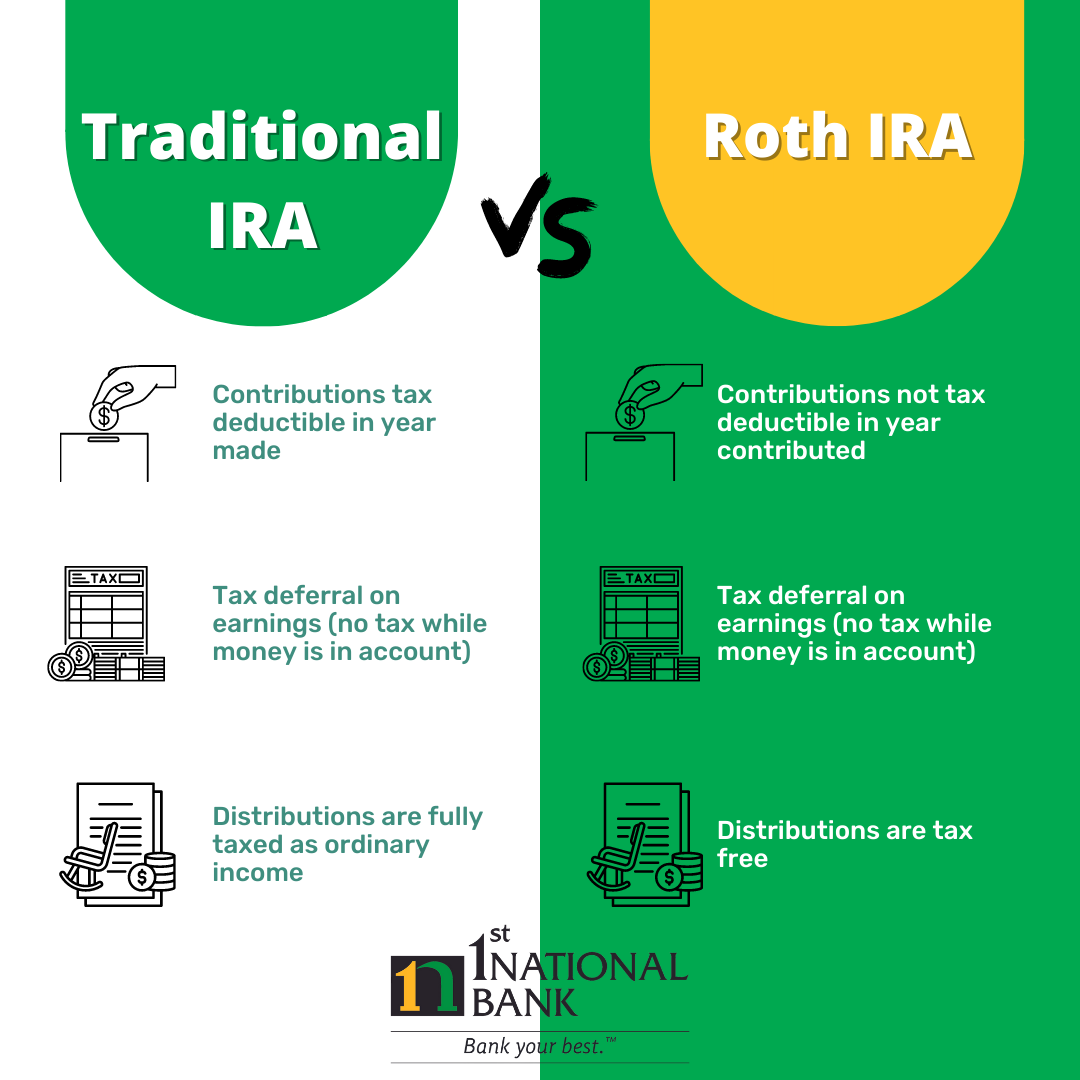

Historically, Traditional IRAs have been favored by individuals expecting to be in a lower tax bracket during retirement than they are during their working years. The contributions are tax-deductible, reducing current taxable income. However, withdrawals in retirement are taxed as ordinary income. Conversely, Roth IRAs offer tax-free withdrawals in retirement. Contributions are not tax-deductible, but qualified distributions (after age 59 1/2 and meeting certain holding periods) are tax-free, representing a significant advantage for those anticipating higher tax brackets in retirement. This makes long-term financial planning critical; predictions about future tax rates inherently involve uncertainty.

This article will delve into the key distinctions between Roth and Traditional IRAs, providing a framework for determining which type is more suitable for specific financial profiles in 2025 and beyond.

FAQs about Choosing Between a Roth and Traditional IRA in 2025

This section addresses frequently asked questions to clarify common uncertainties regarding Roth and Traditional IRA selection.

Question 1: What are the contribution limits for Roth and Traditional IRAs in 2025?

Contribution limits are subject to annual adjustments based on inflation. It's essential to consult the official IRS guidelines for the most up-to-date figures. These limits often differ based on age (those 50 and older typically have a higher contribution limit).

Question 2: Can I convert from a Traditional IRA to a Roth IRA?

Yes, IRA rollovers and conversions are possible. However, conversions are taxed on the amount converted in the year of conversion. Careful consideration of the tax implications is crucial before undertaking a conversion.

Question 3: What happens if I withdraw from my IRA before age 59 1/2?

Early withdrawals from both Traditional and Roth IRAs generally incur penalties unless specific exceptions apply (e.g., first-time homebuyer expenses, qualified higher education expenses). The tax implications also vary significantly depending on the type of IRA.

Question 4: Are there income limitations for contributing to a Roth IRA?

Yes, there are modified adjusted gross income (MAGI) limits for contributing to a Roth IRA. If income exceeds these limits, contributions may be reduced or prohibited. These limits are adjusted annually.

Question 5: How do I choose between a Roth and Traditional IRA if I'm unsure about my future tax bracket?

This scenario often requires a detailed projection of future income and tax rates. Consulting a financial advisor can provide personalized guidance based on your unique circumstances.

Question 6: What is the role of diversification within my IRA?

Regardless of whether you choose a Roth or Traditional IRA, diversification across different asset classes (stocks, bonds, real estate, etc.) is crucial to mitigate risk and potentially optimize returns. This should be a part of a broader investment strategy.

Understanding the answers to these frequently asked questions is a critical first step in making an informed decision about which type of IRA to choose.

Tips for Choosing Between a Roth and Traditional IRA in 2025

Making the right choice requires careful consideration of several factors. These tips offer practical guidance for navigating this important financial decision.

Tip 1: Project your future tax bracket. Carefully estimate your tax bracket during retirement. Will it be higher or lower than your current bracket? This is a key determinant in the decision-making process.

Tip 2: Consider your risk tolerance. Roth IRAs generally involve a higher upfront cost, as contributions are not tax-deductible. This could affect risk tolerance.

Tip 3: Account for potential future income changes. Life events (career changes, inheritance, etc.) can significantly alter your income trajectory. Consider such potential changes in your projections.

Tip 4: Seek professional advice. A qualified financial advisor can provide personalized guidance based on your individual circumstances and risk tolerance.

Tip 5: Review your current financial situation. Assess your current income, expenses, and savings to better understand your capacity for retirement contributions.

Tip 6: Explore the potential tax benefits of each option. Carefully weigh the tax advantages of tax-deductible contributions (Traditional IRA) versus tax-free withdrawals (Roth IRA).

Tip 7: Understand the rules and regulations. Familiarize yourself with the rules governing both Roth and Traditional IRAs to avoid potential penalties.

Following these tips significantly enhances the likelihood of making an informed and beneficial choice for long-term retirement security.

Conclusion on Choosing Between a Roth and Traditional IRA in 2025

The decision of whether to utilize a Roth or Traditional IRA in 2025 hinges on a careful evaluation of individual financial circumstances, projected tax brackets, and long-term financial goals. Understanding the key differences – tax-deductible contributions versus tax-free withdrawals – is paramount. The process necessitates projecting future income and tax rates, a task that often benefits from professional financial guidance.

Ultimately, the optimal choice is not universally applicable but rather depends on a comprehensive assessment of individual needs and circumstances. Proactive planning, informed decision-making, and ongoing review of the chosen strategy are critical for maximizing retirement savings and achieving long-term financial well-being. Consulting with a financial professional can provide invaluable support in navigating this important financial decision.

Published on: 2025-05-08T22:22:16.000Z